Gross income, Adjusted Gross Income, taxes to take off, tax brackets – the lingo around taxes can feel like a minefield. This guide takes you through each step of the tax calculation in plain English, with real numbers so you can see step by step exactly how the math works.

Taxes always make you feel like the simplest numbers should be easy enough but sometimes, somehow, they end up feeling like a complete mess. Yet the actual process of figuring out your taxable income – the number the IRS really uses to calculate your tax bill – is actually pretty straightforward once you break it down. And if you understand each step, you’ll be able to plan ahead, catch some of those sneaky deductions you might have otherwise missed, and avoid those pesky errors that are just waiting to get the IRS’ attention.

This guide runs the whole tax process from start to finish: from adding up every single penny you took in to landing on that final number the IRS is actually working with, with a real life example showing it all in action with each step. Our free checklist for tax preparation is a useful companion to have open alongside this guide.

What is Taxable Income?

Your taxable income is not the same as the number you see on your offer letter – it’s the amount left over after you’ve taken away all the things you legally don’t have to pay tax on. The IRS looks at this number when figuring out your tax bill, not the gross amount on your paycheck – which is why cutting down on that number through things like charitable donations really can save you some cash.

Taxable income is made up of both the income you earn from a job (or freelance work) and the money you get from things like dividends, stock dividends, or any rent you get from property. Unless there’s some special rule that says not to, it’s pretty safe to assume that just about all types of income are included.

Your taxable income is the foundation of your entire tax return. Get this number right and everything else follows with far less friction.

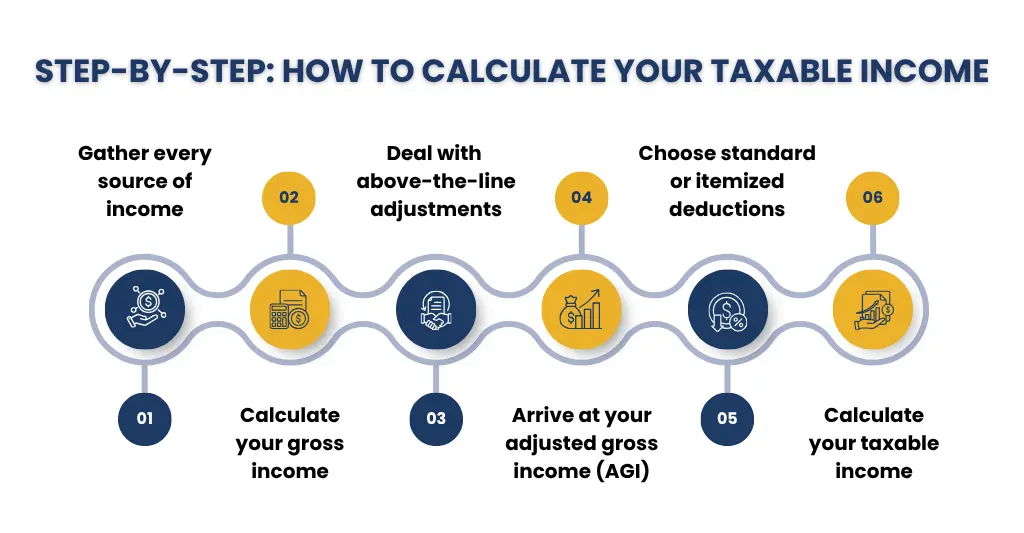

Step-by-step: how to calculate your taxable income

1.Gather every source of income

Collect up those W2s , 1099 NEC forms and 1099 INT statements along with any scribbled down records of cash income . That’s just about anything that’s counted as a source of income – wages, freelance earnings, rental income, interest on the bank, dividends , capital gains, and that taxable bit in the pension pot – not to mention the interest on student loans. Even if you earned cash for some work or investment and didn’t get a proper tax form, it’s still worth including.

2.Calculate your gross income

Just add up all of your taxable income sources – the total is your gross income – before you even think about deducting anything. Business owners might like to deduct ordinary and necessary business expenses first, in which case the profit comes into your personal gross income. See how our business income tax services help owners get this figure right from the start.

3.Deal with above-the-line adjustments

There are some deductions that reduce your gross income right from the get go, even before you make a decision about standard or itemized deductions. These “above the line” adjustments – which show up on Schedule 1 – include contributions to a traditional IRA, HSA contributions, self-employed health insurance premiums, student loans interest and SEP-IRA contributions.

4.Arrive at your adjusted gross income (AGI)

Your Gross Income minus the above-the-line adjustments will give you your Adjusted Gross Income. This is a big deal because it decides whether you qualify for various other credits and deductions, and gets written down on line 11 of your Form 1040.

5.Choose standard or itemized deductions

Now you need to take your AGI and subtract either the standard deduction (a fixed amount that’s based on how you file) or your itemized deductions – whichever is the bigger one. Itemized deductions can include mortgage interest, state and local taxes (although these are subject to the SALT cap), charitable contributions & medical expenses that qualify. You can only choose one option.

6.Calculate your taxable income

Subtract your chosen deduction from your AGI. The result is your taxable income — the number applied to the federal tax brackets to determine your base tax liability, before any credits are applied.

Taxable vs Non-taxable Income – Know the Difference

One of the most common mistakes people make when filing their tax returns is getting income classification wrong. The IRS is going to tax most of your income, but there are a few categories that are either partially or completely exempt from being taxed:

- Income You Definitely Owe Taxes On: W-2 wages, freelancing income, rental income, capital gains, dividend earnings, and interest from your bank account.

- Income You Generally Don’t Owe Taxes On: Life insurance payouts you get if someone passes away, money that comes out of a Roth IRA that you set up and followed the rules for, child support that you receive in the divorce, and most of the gifts you get.

- Some Income Falls in Between: Social Security benefits (it depends on your income overall), interest from municipal bonds (federally it’s exempt but your state might charge tax on it), and some retirement distributions – these often involve complicated calculations and sometimes are taxable, sometimes not.

The rule is simple: if you are unsure, assume it is taxable and verify against IRS guidelines rather than the other way around. Homeowners often ask about property taxes in particular — read our detailed breakdown of the property tax deduction and how to claim it correctly.

Common mistakes to avoid

Not declaring all of your income – whether that’s 1099s, W-2s or a bunch of cash in a drawer. The IRS really doesn’t care where the money came from, just that you report it. That includes payments from people who paid you less than $600, some cash transactions, and earnings from abroad.

- Forgetting about side hustle income: If you get paid to freelance, rent out a room on Airbnb, or sell stuff online, the IRS is getting smarter at tracking that and yes, it’s all taxable. see our overview of costly multistate tax mistakes and how to avoid them.

- Assuming your retirement income is tax free: Don’t get it twisted, the money you withdraw from traditional IRA and 401(k)s is usually fully taxable, and even Roth distributions may be tax free – but only after you’ve met certain requirements.

- Choosing the wrong deduction strategy: Lots of people default to just taking the standard deduction without checking if itemizing would save them more, especially if they’re a homeowner with a big mortgage

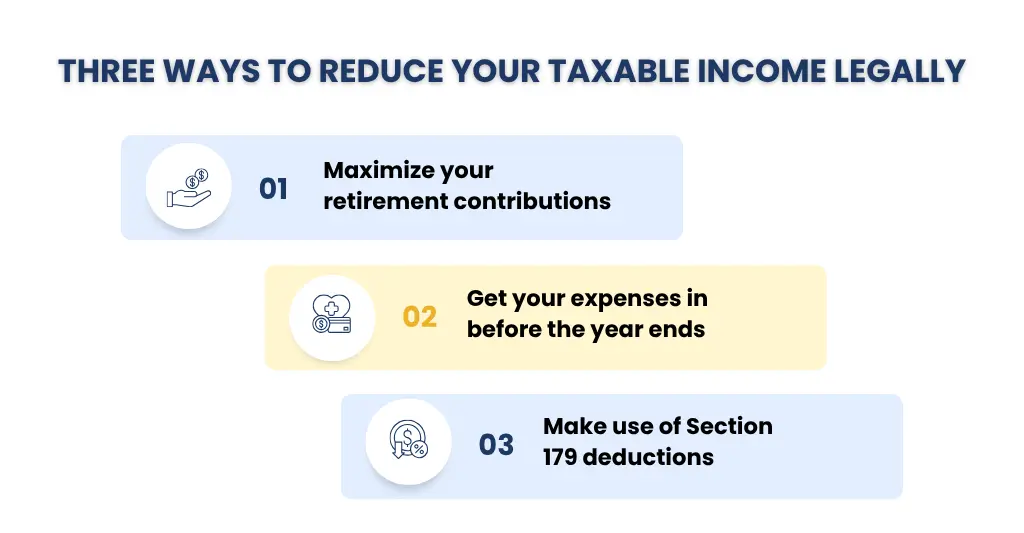

Three ways to legally reduce your taxable income

Tax planning is not about hiding income. It is about making full use of the provisions Congress has already built into the tax code. For a broader playbook, our guide to top tax strategies for maximizing deductions in 2026 covers fifteen techniques across different income types and business structures.

1.Maximize your retirement contributions

Putting money into a Traditional 401(k) or IRA cuts your gross income by the same amount, up to the annual limit. So if you contribute 10,000 dollars, you might just get bumped down to a lower tax bracket.

2.Get your expenses in before the year ends

Pay any business expenses as soon as you can in December and if you can, delay sending out invoices until January. This shifts your taxable income into the next year.

3.Make use of Section 179 deductions

Business owners can write off the full cost of qualifying equipment and gear in the year they buy it, rather than spreading the cost over several years.

How your taxable income connects to your tax bracket

The U.S. uses a progressive tax system, meaning only the income within each bracket is taxed at that bracket’s rate. If Alex’s taxable income is $77,000, a portion is taxed at 10%, another portion at 12%, and the remainder at 22%. No dollar is taxed at a rate higher than the bracket it falls into — a common misconception that causes unnecessary anxiety around earning more.

Once you’ve calculated your base tax from the income brackets, then tax credits kick in and start whittling that number down dollar by dollar. The Child Tax Credit, Earned Income Tax Credit, and education credits are among the most effective ones to have on your side. Now, here’s the key difference: deductions bring your taxable income down but credits directly slash the actual amount you owe. Both are important, but they work at different times in the process. The IRS puts out Publication 505 (Tax Withholding and Estimated Tax) which essentially explains all this in a way that’s pretty clear about how these two play off each other. If you’d like someone to go through all this with you and figure out exactly where you stand, then our financial planning and advisory services would be a good place for you to start.

Not sure you’ve got it right?

Our team at E2E Accounting reviews your income sources, identifies every deduction you qualify for, and ensures your taxable income is calculated accurately — before you file.

FAQs: Frequently Asked Questions

Do bonuses and side income count as taxable income?

Yes. Bonuses are treated as ordinary income and are subject to federal income tax, Social Security, and Medicare taxes. Freelance and gig income must also be reported, regardless of amount — even if no 1099 was issued.

Is investment income included in taxable income?

Generally yes. Interest, dividends, and capital gains are all taxable. Qualified dividends and long-term capital gains may benefit from lower preferential rates, but they still factor into your taxable income calculation.

Can mistakes in my taxable income calculation cause IRS problems?

Yes. Underreporting income, overlooking taxable items, or claiming ineligible deductions can trigger IRS notices, penalties, and interest. In cases of significant underreporting, an audit may follow. Accurate records and a systematic approach are the best prevention.

What deductions reduce taxable income the most?

For most individuals, the standard deduction, retirement account contributions, and HSA contributions are the most impactful. For homeowners and high-income earners, itemized deductions — particularly mortgage interest — can exceed the standard deduction significantly.

Conclusion :

Calculating your taxable income is a six-step process: gather all income, determine gross income, apply above-the-line adjustments to reach your AGI, choose the larger of standard or itemized deductions, subtract it, and arrive at taxable income. Each step is an opportunity to reduce what you owe — legally and intentionally.

The most costly tax mistakes are rarely complex schemes. They are missed deductions, unreported side income, and assumptions about what is or is not taxable. A clear understanding of how the calculation works is the first line of defense against both overpaying and underpaying.

If your income situation has grown more complex — multiple income streams, a side business, or significant investments — working with a qualified accountant ensures nothing falls through the cracks. Our tax preparation services are built for exactly this kind of situation, handling the full calculation from gross income to final filing.