Consider a small marketing agency in Texas preparing its year-end tax returns. The owner assumes the calculations are simple: income minus expenses, submit the return, and move on. But, while checking the accounts, the accountant sees something significant. During the year, the company purchased new laptops for its employees, invested in marketing tools, and paid for professional training.

None of these were correctly classified as tax deductions.

After applying the appropriate deductions, the company’s taxable income decreased dramatically, saving thousands of dollars in taxes. Situations like this are more common than you may believe. Many US firms focus on running their operations year-round, but when tax season hits, they forget significant deductions. As a result, they pay more taxes than necessary.

Year-end tax planning includes not only filing forms on schedule, but also ensuring that your company claims every lawful deduction allowed by IRS rules. In this blog, we will go over the essential year-end deductions that US businesses should consider before filing taxes, allowing you to lower your tax liability while remaining fully compliant.

What Is a Tax Deduction (and What Is a Tax Write-Off)?

A tax deduction is a business expense that lowers your company’s taxable income. Businesses that claim qualified expenses might reduce their taxable income and, as a result, their tax burden.

For example,

if a company earns $100,000 and has $30,000 in deductible expenses, it will only owe tax on $70,000.

A tax write-off is merely another name for the same concept. Businesses “write off” expenses as a tax deduction.

However, the IRS only allows deductions for typical and required company expenses, such as rent, software, marketing, or professional services.

The Real Cost of Waiting Until April, How to get more on tax return?

Many business owners wait until April to consider taxes, but by then, the majority of possibilities to lower your tax payment may have passed. Tax planning is most effective before the end of the year, rather than when the return is ready to be filed.

For example,

if a company waits until April to file its taxes, it may miss out on deductions for equipment purchases, retirement contributions, bonus payments, and prepaid business costs. To qualify for deductions, these actions must typically be done before the end of the financial year.

Businesses that plan ahead of time might legitimately cut their taxable income and enhance their net profit.

To maximize the tax return, firms should:

- Review all business expenses and deductions before filing.

- Ensure that equipment, software, and operational costs are accurately recorded.

- Maximize retirement contributions and business credits.

- Work with an accountant to find missed deductions.

Waiting until the last minute usually results in paying more tax than necessary. Early planning enables businesses to claim all available deductions and retain more of their profits.

What is a Tax Credit vs Tax deduction?

| Feature | Tax Deduction | Tax Credit |

| Meaning | Reduces the amount of income that is taxed. | Directly reduces the tax you owe |

| Impact on Taxes | Lowers taxable income | Lowers the total tax bill. |

| Financial Benefit | Depends on your tax rate. | Full value reduces tax liability. |

| Example | Business expenses like rent, software, salaries | R&D tax credit, energy efficiency credits |

| When Applied | Before calculating the final tax. | Applied after calculating tax owed |

When Should Businesses Plan for Deductions? (Hint: Not in April)

The most common mistake firms make is the sit for tax planning a few days before the deadline. Unfortunately, by that time, most opportunities to lower taxable income had passed. An exam can be cracked studying before a few days, but for tax filing you have to be punctual.

The ideal duration to plan for deductions is throughout the year, particularly in the fourth quarter (October-December), when firms can still take steps to reduce their tax liability.

For example, businesses may decide to:

- Purchase the equipment or software required for operations.

- Pay some company expenses in advance.

- Contribute to retirement plans.

- Record and organize all deductible business costs.

Instead of scrambling at the last minute, businesses may plan ahead of time and make wise financial decisions. Businesses can use appropriate year-end tax preparation to claim all applicable deductions, lower taxable revenue, and avoid paying more tax than necessary.

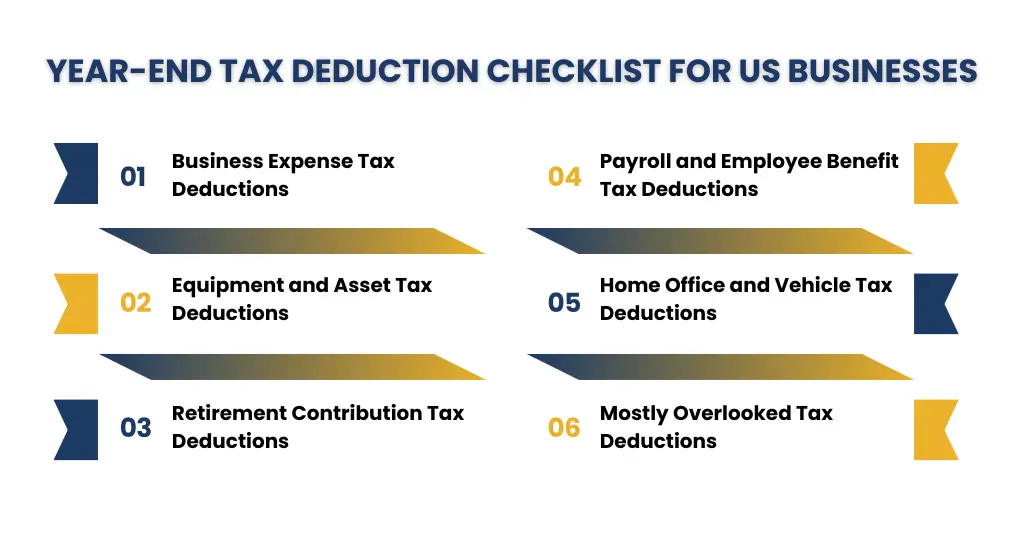

Year-End Tax Deduction Checklist for US Businesses

As the financial year comes to an end, examining your costs and financial decisions can guarantee that your company takes advantage of all possible IRS deductions. Many businesses miss out on important deductions simply because they do not thoroughly analyze their records before tax filing.

Use the below given checklist to discover typical deductions that can help lower your taxable income.

Business Expense Tax Deductions:

Most regular operational costs may be tax deductible if they are ordinary and necessary for running your firm.

Common deductible expenses include:

- Office rent or coworking space

- Software subscriptions and SaaS tools

- Marketing and advertising costs

- Professional services such as accounting or legal fees

- Office supplies and internet expenses

Keeping accurate records of these expenses throughout the year ensures that they are correctly claimed on tax returns.

Equipment and Asset Tax Deductions — Section 179 and Bonus Depreciation

Businesses that purchase equipment, machinery, computers, or other assets may be able to deduct a significant amount of the cost in the same year using Section 179 or bonus depreciation.

End of year business tax deductions enable businesses to recover the cost of qualified assets more quickly rather than spreading the deduction over multiple years.

Examples include:

- Computers and laptops

- Machinery and manufacturing equipment

- Office furniture

- Certain vehicles used for business

Reviewing major purchases before filing taxes can help maximize these deductions.

Retirement Contribution Tax Deductions:

Contributions to retirement plans can provide large tax breaks while also helping business owners and employees save for the future.

Common deductible retirement contributions include:

- SEP-IRA contributions

- SIMPLE IRA plans

- Solo 401(k) contributions

These contributions can minimize taxable income while also improving the company’s long-term financial planning capabilities.

Payroll and Employee Benefit Tax Deductions:

Employee expenses are frequently among the largest deductions available to organizations. These fees could include:

- Employee salaries and wages

- Payroll taxes paid by the employer

- Health insurance contributions

- Retirement plan contributions for employees

- Bonuses and performance incentives

Ensuring that all payroll-related costs are appropriately recorded can help firms claim the maximum deduction possible.

Home Office and Vehicle Tax Deductions:

Business owners who work from home or drive a vehicle for business purposes may be eligible for additional deductions.

Examples are:

- Home office expenses, including a part of rent, utilities, and internet

- Mileage or actual automobile costs for business trips

- Parking fines and tolls associated with commercial activity

Maintaining adequate records or mileage logs is critical to supporting these deductions if the IRS conducts an audit.

Mostly Overlooked Tax Deductions:

Some end of year tax deductions that are frequently missed because businesses may not realize they qualify.

Examples include:

- Business insurance premiums

- Bank fees and payment processing charges

- Education and professional training costs

- Subscription services used for business operations

- Business travel and certain meal expenses

Reviewing financial records before filing taxes can assist discover these missing deductions and prevent the company from paying more tax than necessary.

What Expenses Don’t Qualify as a Deduction? ( Simple example)

Not all business expenses can be claimed as tax deductions. The IRS only allows costs that are usual and necessary for conducting business. Expenses that are personal or unrelated to business activity are normally not deductible.

Some common expenses that usually do not qualify as tax deductions include:

- Personal living expenses

- Personal travel or vacations

- Clothing that can be worn outside of work

- Fines or penalties paid to government authorities

- Commuting costs from home to a regular workplace

Understanding which expenses are not deductible assists firms in avoiding errors, lowering the risk of IRS difficulties, and maintaining proper tax returns.

How Your Tax Bracket Affects Every Deduction You Claim?

Your tax bracket impacts how much advantage you get from each tax deduction. Deductions reduce your taxable income, thus your actual savings are determined by the tax rate applied to that income.

For example,

if your business claims a $10,000 deduction:

- In a 30% tax bracket, you could save about $3,000 in taxes.

- In a 20% tax bracket, the same deduction would save about $2,000.

This means that deductions are often more advantageous for firms in higher tax levels, as each dollar deducted cuts more taxes.

Understanding your tax bracket enables firms to make better decisions regarding timing costs, investments, and deductions. Businesses that plan ahead of time can optimize tax savings and keep more of their profits.

Top Tax Deduction Mistakes Businesses Make

Here are some mistakes listed down:

- Missing Legitimate Deductions: Some organizations fail to manage expenses, ignore deductions such as software subscriptions, bank fees, professional services, and training charges.

- Mixing Personal and Business Expenses: Using the same bank account or credit card for personal and professional expenses might cause confusion and result in improper deductions.

- Poor Record Keeping: Claiming deductions without sufficient paperwork, such as receipts, invoices, or mileage logs, might result in complications if the IRS requires verification.

- Misunderstanding Asset Deductions: Many organizations mistakenly expense major items that should be depreciated, or they do not take advantage of potential benefits such as Section 179 or bonus depreciation.

- Waiting Until the Last Minute: Reviewing spending solely when filing taxes frequently results in missing deductions and hurried financial decisions.

How Clean Books Unlock Maximum Tax Deductions, How can I get the biggest tax refund?

Accurate bookkeeping is essential for optimizing tax deductions. When financial records are clean and organized, it is easier to discover all allowable business expenses before filing taxes.

Businesses that keep their accounts updated, can easily manage deductions like software charges, marketing expenses, equipment purchases, and payroll costs. Many of these deductions may go undetected if proper records are not kept.

How Can You Get the Biggest Tax Refund?

- Keep books updated throughout the year

- Track all business expenses properly

- Separate personal and business transactions

- Review deductions before filing taxes

Clean books help ensure businesses claim every eligible deduction and reduce their tax bill.

How E2E Accounting Helps Businesses Identify More Tax Deductions — Before It’s Too Late

Several companies lose important deductions simply because their books are not checked on time. E2E Accounting assists firms in identifying deductible items early, ensuring that nothing is neglected prior to tax filing.

The financial documents are reviewed by my employees; appropriate documents are compiled; and we search available business deductions (e.g., business-related expenses, purchases of capital assets, payroll) to identify potential tax deductions that may be available for you or your business.

E2E Accounting helps companies minimize their taxable income while being compliant with applicable IRS regulations by providing accurate accounting records, timely reporting on financial results and correctly classifying expenses to ensure the best possible tax outcome.

Instead of rushing through tax season, businesses may plan ahead of time, maximize deductions, and avoid paying more than required.

Don’t Wait Until April — Build a Deduction Strategy Now

Waiting until April is not a right decision as it frequently results in missed opportunities to minimize your tax bill. The best tax savings come from year-round planning rather than just filing your return.

Businesses can dramatically reduce their taxable revenue by assessing spending early, tracking deductions, and making strategic financial decisions before the end of the financial year.

Start building a deduction strategy by:

- Reviewing business expenses regularly

- Recording and categorizing transactions accurately

- Planning major purchases before year-end

- Working with accounting experts to identify overlooked deductions

A proactive approach allows firms to optimize deductions, remain compliant, and retain more of their revenues.

Stop Overpaying on Taxes — Let E2E Accounting Find What You’re Missing

Our team reviews your books, identifies every eligible deduction, and ensures you’re fully compliant before the deadline hits.

FAQs : Frequently Ask Question

How early should I start planning my business tax deductions?

You should prepare your business tax deductions at the start of the year and examine them on a regular basis. Most organizations conduct a thorough examination in the last quarter (October-December) to identify expenses and deductions prior to the end of the financial year. Early planning allows you to optimize your tax savings while also avoiding missing out on crucial deductions.

What tax deductions can I claim?

Office rent and utilities

Software and subscriptions

Employee salaries and payroll taxes

Marketing and advertising costs

Equipment and business assets

These deductions help reduce taxable income and lower the total tax you owe.

Are tax deductions different for LLCs and S-Corps?

Yes, most tax deductions are the same for LLCs and S-Corps, such as rent, payroll, software, marketing, and equipment expenses.

The main difference is how owner income is treated.

1.LLCs usually report profits on the owner’s personal tax return.

2.S-Corps require owners to take a reasonable salary, with additional profits taken as distributions.

What new tax deductions are introduced under the One Big Beautiful Bill Act (OBBBA)?

The One Big Beautiful Bill Act (OBBBA) added and enhanced various tax breaks for people and corporations.

Key deductions include:

The SALT deduction cap has been increased from $10,000 to $40,000 for qualifying taxpayers.

Employees can deduct up to $25,000 in eligible tips.

Deduction for overtime pay is up to $12,500 ($25,000 for couples).

Individuals over the age of 65 can claim a tax deduction of up to $6,000.

Non-itemizers can claim a charitable deduction of up to $1,000.

Increased business deductions for equipment purchases and research investments.

These measures seek to lower taxable income while encouraging corporate investment and workforce earnings.

Conclusion

Tax season doesn’t mean paying more than necessary. Businesses can lower taxable income and increase cash flow by recognizing potential deductions and planning ahead of time.

The trick is to not wait until the deadline in April. Businesses that keep reliable records, examine spending on a regular basis, and schedule deductions before the end of the year are more likely to obtain all eligible tax benefits.

Businesses may stay compliant with IRS requirements while making smarter financial decisions and keeping more of their hard-earned income if they use the right approach and bookkeeping.