Property Taxes – A Big Chunk Out of Your Pocket Every Year

You write a lot of big cheques as a homeowner, and the last thing you want to do is miss out on a deduction or worse, get the IRS lining up to take a closer look at your tax return. In this guide, we’ll take you through everything you need to know about claiming a property tax deduction properly – from understanding this SALT thing to knowing what you can and can’t actually claim.

Tax professionals, misclassification or incomplete documentation can trigger client exposure and reputational risk. This guide covers the rules as they stand, so your advice stays on solid ground

How Property Taxes Impact Your Tax Return

For homeowners, one of the easiest ways to whittle down your federal tax bill is by getting your property tax deduction right on schedule A (Form 1040). But it’s not just about scribbling down a number – you need to keep on top of things, classifying and documenting everything correctly, so you don’t have to deal with the headache of an audit.

| Category | Detail | Note |

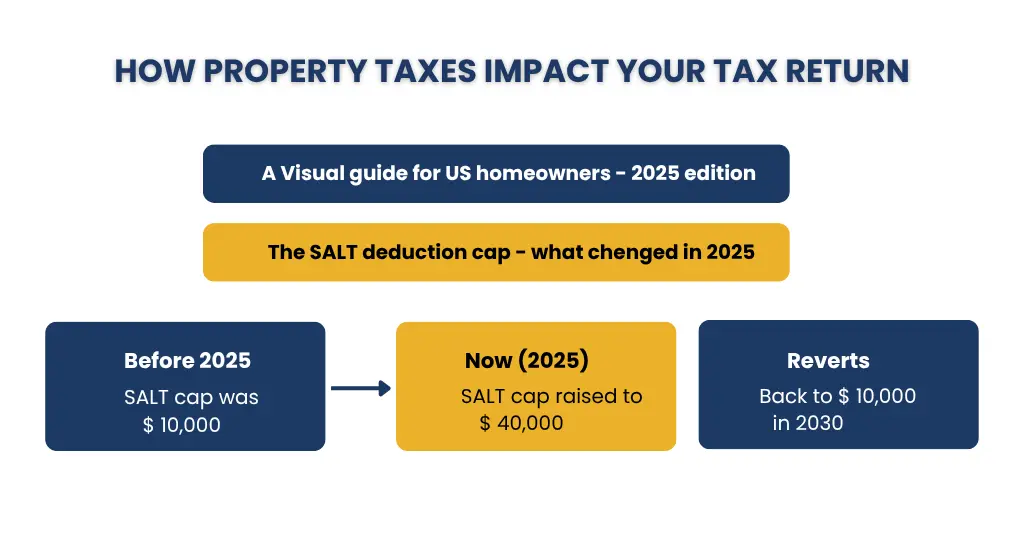

| SALT Deduction Cap (2025) | ||

| What it covers | State & local taxes, incl. property taxes | Schedule A |

| Standard cap (most filers) | $40,000 | 2025 rate |

| Married filing separately | $20,000 | 2025 rate |

| Effective date of new law | July 4, 2025 | — |

| Annual cap increase | 1% per year | Through 2029 |

| Cap reverts to | $10,000 | From 2030 |

| High Earner Rules | ||

| MAGI threshold | $500,000 or more | Phase-out begins |

| Impact above threshold | Cap is reduced | 30 cents per dollar over limit |

| Minimum cap (high earners) | $10,000 | Floor — never lower |

| Itemizing Requirement | ||

| Condition to claim deduction | Must itemize on Schedule A | — |

| What counts toward total | Property taxes + mortgage interest + charitable donations | Combined total |

| 2025 Standard Deduction | ||

| Single filers | $15,750 | Must beat this to itemize |

| Married filing jointly | $31,500 | Must beat this to itemize |

If you’re going to get any benefit from the property tax deduction at all, you need to itemize – and that means your total itemized deductions (property taxes, mortgage interest, charitable donations, etc.) need to be more than the standard deduction for this year – which is $15,750 for single people and $31,500 for couples filing jointly.

How Much Property Tax You Can Actually Deduct?

You can write off the property taxes you actually laid out for during the year on your primary or second home to state or local governments, up to that $40,000 SALT cap for 2025.

Here are a few things to take into account. The only payments you can deduct are the ones you actually paid – not some unpaid bill or a rough estimate. If your mortgage lender is paying property taxes through that escrow account, you can only claim what they actually sent to the tax collector, not what extra cash you tossed into the account each month. Your Form 1098 from your lender will give you the lowdown on just how much they paid out. And by the way, if you’ve got a MAGI over $500,000, your deduction is going to start getting phased out at the rate of 30 cents for every dollar you go over that.

When you claim this alongside your mortgage interest and charitable deductions it really can help take a good chunk off what you owe.

Which Property Taxes Are Okay to Claim – and Which Aren’t

Not everything on your tax bill gets to be deducted, and that’s where a lot of homeowners end up tripping over their own feet.

You can write off state and local real estate taxes based on your property’s assessed value that are meant to help out the general public (these taxes are the standard property taxes your county or municipality slaps on every year)

You cannot deduct special assessments for local improvements that directly benefit and increase the value of your property — things like new sidewalks, sewer lines, streetlights, or water mains. These aren’t taxes in the traditional sense; they’re charges for specific improvements. Similarly, service fees like trash collection, water usage charges, or lawn maintenance notices from your local government are not deductible.

When in doubt, look at whether the charge is based on your property’s value (likely deductible) or tied to a specific service or improvement (likely not).

Property Tax Deductions: Primary Homes vs. Rental Properties

At first glance, property tax deductions seem simple — you pay the bill, you deduct it. But once you own multiple properties, have a mixed-use rental, or start approaching the SALT limit, things get more nuanced. Here’s how it breaks down.

| Feature | Primary Home (Schedule A) | Rental Property (Schedule E) |

| Deduction Form | Schedule A | Schedule E |

| Deduction Type | Itemized deduction | Business expense |

| SALT Cap Applies? | Yes | No |

| 2025 SALT Cap | $40,000 ($20,000 if MFS) | No limit |

| Deduct Full Amount? | No (capped) | Yes |

| What Qualifies? | Taxes based on assessed value only | Full property tax as a business expense |

| Special Assessments? | Not deductible | Deductible as expense |

| Deducted Against | Overall taxable income | Rental income |

| Personal Use Required? | Yes – primary residence | No personal use allowed |

Know More: Property Management Accounting Explained: What Every Landlord Should Know

For mixed-use properties — where you both live in and rent out part of the same building — you’ll need to split the property tax between personal use and rental use, typically based on proportional square footage. The rental share goes on Schedule E with no cap; the personal share goes on Schedule A subject to the SALT limit.

Keeping Your Records Clean

If you own multiple properties, staying organized by property, entity, and tax year isn’t optional — it’s essential. Clean records make filing easier, keep you audit-ready, and make sure you’re capturing every deduction you’re entitled to without accidentally mixing up personal and business expenses.

Documents You Need to Get Your Property Tax Deductions

Before you even think about filing, make sure you’ve got these in your hands first:

The Essentials to Grab:

- County tax bills and the payment receipts that prove you paid your local tax authority during the year.

- Your mortgage lender’s Form 1098 – that’s the one that shows how much of your property taxes got paid out of your escrow account (if that’s how it works for you).

- Your bank or escrow statements that back up the exact dates and amounts you paid – not just guesses.

Keeping Track for Your Own Safety

Keep a clear record of which bits are property taxes and which bits are non-deductible service fees or special assessments that’ll get you into trouble if you get audited. If you’ve got a high income and in danger of hitting the $500,000 MAGI limit where your SALT deductions get phased out, make sure you track exactly how much you paid – it really does matter. And each year, compare your itemized deductions to the standard one to see which one gives you a lower tax bill.

How to Choose: Itemize Deductions or Take the Standard Deduction?

Not sure which route is right for you? Here’s a quick side-by-side breakdown to help you decide in seconds:

| What to Consider | Standard Deduction | Itemized Deduction |

| How Easy Is It? | Very easy — no receipts or paperwork needed | More work — track and document everything |

| 2025 Single Filer Amount | $15,750 | Depends on your actual expenses |

| 2025 Married Filing Jointly | $31,500 | Depends on your actual expenses |

| 2025 Head of Household | $23,625 | Depends on your actual expenses |

| What Counts? | Fixed IRS amount — nothing to add up | Mortgage interest, property taxes, charity, medical expenses over 7.5% AGI |

| SALT Cap | Not applicable | $40,000 limit in 2025 |

| Who Uses It? | ~88–90% of Americans | Homeowners with big mortgages or high property taxes |

| Audit Risk | Very low | Slightly higher — keep your documents |

| Form Needed | Form 1040 only | Form 1040 + Schedule A |

| Best For | Expenses less than standard amount | Expenses more than standard amount |

| Bottom Line | Simple, stress-free, works for most people | Worth the effort when your bills are big |

Still unsure? Pull out your Form 1098, add up your mortgage interest, property taxes, and charitable donations — if the total beats your standard deduction amount, itemizing wins every time.

When Property Tax Deductions Get Complicated

When you start to get into multiple properties, rental homes or taxes paid through escrow things can start to get a lot more complicated. Here’s the low down on the most common tricky bits and how to tackle them:

- Escrow payments: Your lender pays your property taxes for you through escrow – but you can only claim what actually got paid out – not the bits you’re putting in each month. Double check your Form 1098 for the exact amount paid.

- Non-deductible fees: HOA fees, trash collection and those types of charges are not property taxes and won’t count towards your SALT.

- When You Part-owned a Property for a Bit of the Year: If you bought or sold a home during the year you can only claim the taxes for the bit of the year you actually owned it. Your closing statement will have the details on the taxes being prorated – that’s important to get right.

- Claim every exemption: You qualify for. Seniors, veterans, people with disabilities, and homeowners who made energy-efficient improvements may all be eligible for additional exemptions or credits. A quick call to your local tax office can uncover savings you didn’t know existed.

- Vacation homes and foreign properties: These have their own tracking requirements. Vacation home deductions depend heavily on how many days the property was used personally versus rented out.

- Alternative Minimum Tax (AMT): If you’re subject to AMT, property tax deductions work differently. It’s worth talking to a CPA if this applies to you.

When to Reconsider Your Property Tax Deductions Before Filing

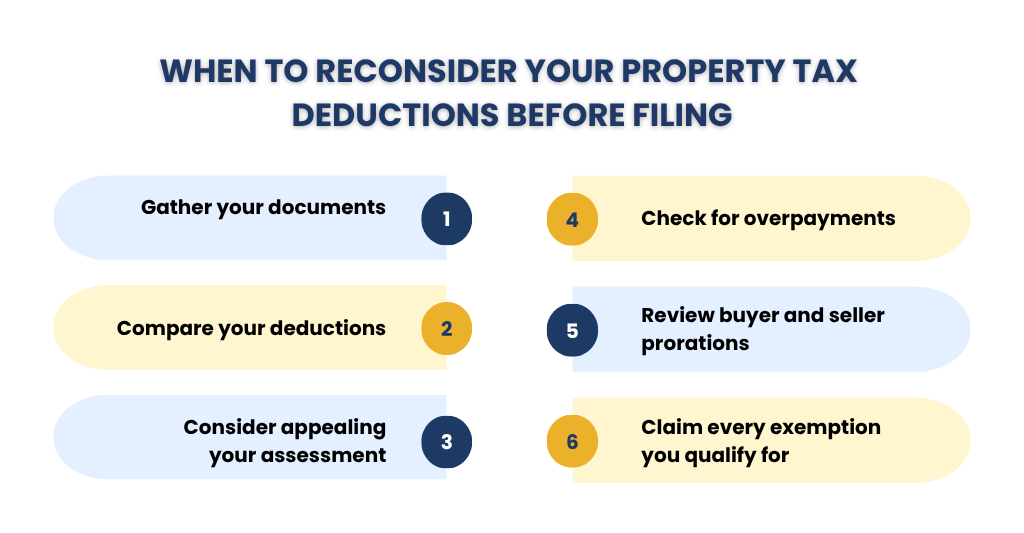

The best time to start reviewing your property tax situation is January — that gives you a comfortable runway before the April 15 deadline, or October 15 if you’ve filed for an extension. Here’s a practical checklist:

- Gather your documents: Collect your Form 1098, county tax bills, and payment receipts before you sit down to file.

- Compare your deductions: Use a tax calculator or software to see whether itemizing beats your standard deduction this year.

- Consider appealing your assessment: If your property tax bill seems too high, most counties give you a 30 to 45-day window from receiving your assessment notice to file an appeal. Bring comparable sales data, photos, or an appraisal as evidence. A successful appeal can lower future bills and may even reduce what you owe retroactively.

- Check for overpayments: Log into your county’s tax portal to see if a billing error or successful appeal has left a credit or refund waiting for you.

- Review buyer and seller prorations: If you bought or sold a home during the year, check your closing statement to confirm you’re claiming the right portion of property taxes.

- Claim every exemption: You qualify for. Seniors, veterans, people with disabilities, and homeowners who made energy-efficient improvements may all be eligible for additional exemptions or credits. A quick call to your local tax office can uncover savings you didn’t know existed.

Common Property Tax Deduction Mistakes Homeowners Make

Even well-intentioned homeowners make these mistakes more often than you’d think.

The most common one is using the wrong payment date. Property taxes are deductible in the year you actually pay them — not the year the bill was issued. If your bill arrived in December but you paid it in January, that deduction belongs to next year’s return.

Another frequent mistake is relying on monthly escrow contributions instead of actual disbursements. What you pay into escrow each month is not the same as what your lender actually paid to the tax authority. Always use your Form 1098 to find the exact disbursed amount.

Homeowners also commonly try to deduct non-deductible charges — HOA fees, trash collection, or sidewalk assessment fees — as property taxes. These simply don’t qualify.

And with the SALT cap now at $40,000 for 2025, make sure you’re using the current figure, not the old $10,000 limit from prior years.

Three Quick Tips to Stay on Track:

• Verify all payments using your tax bills, bank statements, and Form 1098.

• Separate legitimate property taxes from service charges and special assessments.

• Compare your total itemized deductions against the standard deduction every single year — the right answer can change.

Ready to make sure you’re maximizing your property tax deductions? Don’t risk leaving money on the table! Schedule a consultation with our tax experts today and get your property tax filing right.

People Also Ask:

What happens if I claim property tax incorrectly?

The IRS can disallow the deduction, charge a 20% accuracy penalty plus interest, and potentially trigger an audit. If you catch a mistake after filing, you can correct it by filing an amended return on Form 1040-X within three years to limit the damage.

Should I review my property tax deduction before filing?

Absolutely. Verify your documents — Form 1098, county tax bills, and payment receipts — ideally by early February. Double-check your total SALT payments against the current cap, and compare your itemized total to the standard deduction to confirm which approach saves you more.

Is property tax deductible for rental properties?

Yes — and it’s actually better for rental properties. Property taxes on rentals are fully deductible as a business expense on Schedule E with no SALT cap limitation whatsoever. Unlike your primary home, rental property taxes are treated as ordinary business expenses, so there’s no ceiling on what you can deduct.

How much property tax can I deduct in a year?

For your primary home, you can deduct up to the SALT cap — $40,000 for 2025, rising 1% annually through 2029, then reverting to $10,000 in 2030. High earners above $500,000 MAGI face a phase-out. For rental properties, there’s no cap — you deduct the full amount on Schedule E.

What documents do I need to support a property tax deduction?

You’ll need your Form 1098 (which shows escrow disbursements for property taxes), county tax bills and receipts, and your Closing Disclosure if you bought or sold a home during the year.

How do I get my property taxes lowered?

The most effective routes are appealing your assessment with comparable sales data, applying for homestead or senior exemptions, or qualifying for credits tied to energy-efficient home improvements. Even a modest reduction adds up over time.

Conclusion

Getting your property tax deductions right isn’t just about saving money this year — it’s about building habits that protect you every filing season. With the SALT cap at $40,000 for 2025, more homeowners than ever have a real opportunity to benefit from itemizing. But the rules around what qualifies, which schedule to use, and how to document everything properly genuinely matter. Review your situation each year, keep clean records, and don’t hesitate to consult a tax professional if your situation is complex. The few hours you invest in getting this right can be worth thousands of dollars.