It feels unutterable to fall behind on books, but services like catch-up bookkeeping are here to help you clean up your past-due bookkeeping and get current.

Running a business is a tough job, it requires hard work, dedication and consistent effort. With a lack of attention in managing finances, operations and customer service, it’s easy for bookkeeping tasks to slip through the cracks. Due to a lack of in-house resources, time and knowledge, many small to mid-sized businesses fail to maintain their books.

If this sounds familiar, you’re not alone. Catch-up bookkeeping involves recording all missed financial transactions to get your books current and accurate. Whether it’s a few months or a year-long pause, catching up is essential to remain compliant with tax regulations, especially when the tax season is looming nearby.

In this blog, we’ll break down everything you need to know about catch-up bookkeeping—what it is, when you need it, how much it costs, and whether it’s better to handle it yourself or hire a professional.

What Is Catch-Up Bookkeeping?

Catch-Up Bookkeeping is the process of updating and organizing all incomplete financial records to bring your books up to date by recording all untracked transactions.

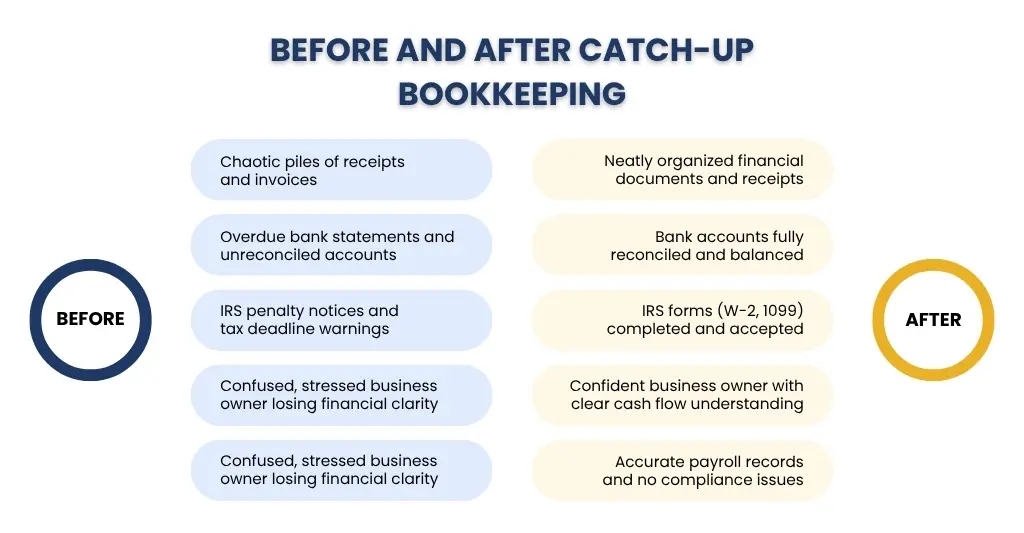

Getting caught up on your books isn’t just about organization—it gives you clarity about understanding your cash flow, making smart financial decisions, preparing for tax season, and presenting accurate financial data to investors, lenders, or auditors to make future decisions. This process may help you find out a financial knot in one of the areas that is holding you back from scaling your business as quickly as you want to.

Of course, prevention is better than a cure and catch-up bookkeeping is a lifesaver, especially for a small to mid-sized business.

Note on US Tax Compliance: Staying updated with your bookkeeping ensures timely filing of IRS forms such as 1099s or W-2s, and adherence to federal and state tax deadlines, helping you avoid costly penalties and audits.

8 Signs You Need Catch-Up Bookkeeping

If you’re a small business owner struggling with a bookkeeping backlog and wondering what can fix the mess hassle-free, catch-up bookkeeping is the solution as it helps you clean up the errors so you can make informed decisions and grow your company confidently.

Here are eight clear signs it’s time to get caught up:

1. Bank accounts overdue for reconciliation for 3+ months

Regular reconciliation helps ensure your books match your actual bank activity. If this hasn’t happened in a while, errors or fraudulent charges could go unnoticed.

2. Having hard time tracking your business profitability

Without up-to-date financial reports, you won’t have a clear picture of your business performance. You won’t know if you’re making a profit or losing money, making it hard to measure success accurately.

3. Your CPA/accountant asking for records constantly

It’s a red flag if your accountant is constantly chasing you down for missing data that means your bookkeeping is falling behind, and tax season could get complicated fast.

4. Missed out on tax deadline

You are facing difficulties with filing taxes which results in penalties and interest. Often, this happens when backlog bookkeeping prevents you from accessing the numbers you need to file accurately.

5. You feel “in the dark” about your business’s financial health

Every business decision feels like a guess as you don’t have a clear picture of your cash flow or financial position. Without updated records the clarity you need to move forward with confidence is missing.

6. Your payroll records are disorganized

Losing track of payroll records can lead to unhappy employees, compliance issues and tax problems. If the records are scattered or incomplete, it’s time to clean up your books.

7. Getting penalties from the IRS

Falling behind on records can result in inaccurate or late tax filings, which often becomes difficult to file returns correctly, increasing the risk of receiving notices or penalty letters from the IRS.

8. Losing crucial financial records

Without regular maintenance of your bookkeeping, important documents can easily get lost and misplaced. This can potentially cost your business time and money, making it harder to verify transactions, support deductions during tax time or respond to audits.

If you experience any of these eight signs, it’s clear your business needs a bookkeeping clean-up. This will help you grow your business while staying compliant.

The Risks of Delaying Catch-Up Bookkeeping

Delaying bookkeeping can result in significant financial losses, impacting various aspects of financial management, including invoicing, payroll, expense tracking, and tax compliance. It also disrupts daily operations and can result in penalties during tax season.

Let’s explore the risk factors you can face if you are behind on your book:

1. Struggling with the IRS Fire

From expensive penalties on federal tax filings to late fees on state tax returns, neglecting bookkeeping can result in significant financial loss for your business. Regulatory alignment becomes seamless when bookkeeping is maintained, ensuring that your business remains in good standing with the IRS and state tax authorities.

2. Shortfall of Hard-Earned Money

Disregarding your bookkeeping is like saying goodbye to your hard-earned money. It impacts various aspects of your financial management, from invoicing and payroll to expense tracking and tax compliance.

3. Financial Clarity Fades Away

Bookkeeping works as the pillar of your company’s financial clarity. The clear image of your finance begins to fade away when it gets neglected, making it challenging to track your cash flow.

4. Dealing with a Pileup of Bookkeeping Tasks

One of the most crucial challenges of ignoring bookkeeping is facing a backlog of financial tasks this leads to pay penalties during tax season and also disrupts your day-to-day operations.

Ignoring bookkeeping will cost a business a lot in the long run, as it acts as a foundation in all aspects of your company’s financial health.

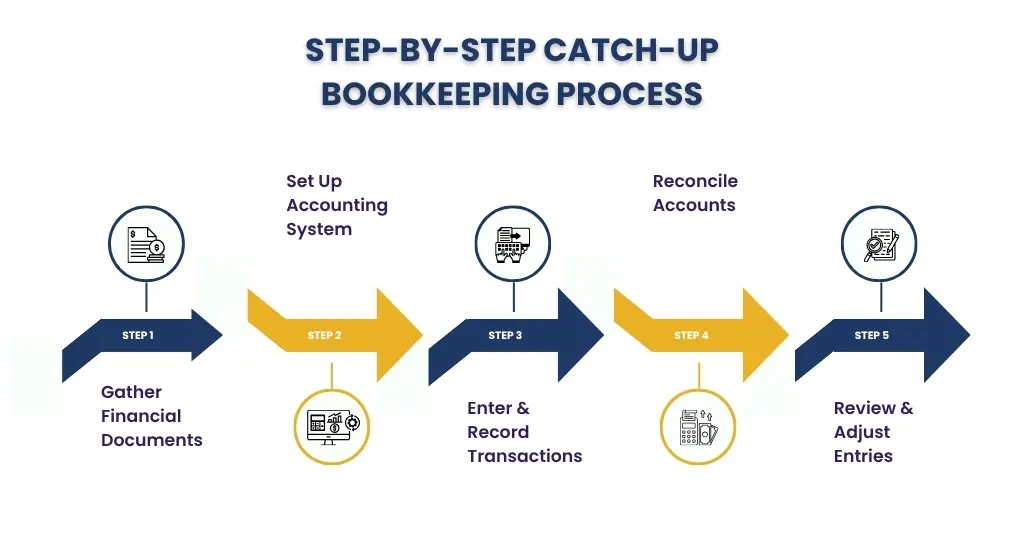

How the Catch-Up Bookkeeping Process Works (Step-by-Step)

Step 1: Gather All Financial Documents

The First step involves the collection of financial documents like bank statements, credit card statements, receipts, invoices, and any previous bookkeeping records.

Step 2: Set Up Your Accounting System

For small to mid-sized businesses, this step includes setting up your accounting system properly using tools like QuickBooks, Xero, and FreshBooks. It also categorizes your income and expenses to reflect your business operations.

Step 3: Enter and Record All Transactions

Bookkeepers systematically work through your financial documents, entering each transaction into your accounting system. This includes chronologically determining the opening balance of your accounts at the beginning of the catch-up period.

Step 4: Reconcile All Accounts

Once all data is entered, next step is reconciling each credit card and bank transaction to ensure everything adds up and matches the real balances, and identify your company’s financial position.

Step 5: Review and Adjust Entries

Before finalizing, the bookkeeper reviews the catch-up work. They check for unusual transactions, missing records, or errors, and make necessary adjustments, such as depreciation or accrued expenses.

DIY vs. Professional Catch-Up Bookkeeping

| Aspects | DIY | Professional Catch-Up |

| Meaning | Business owners or staff handle bookkeeping tasks themselves using tools or software | A trained bookkeeper or firm manages all bookkeeping tasks on behalf of the business |

| Cost | Low cost, but high time investment | Higher cost, but saves time and reduces errors |

| Time Required | Time-consuming, especially for non-bookkeepers | Fast turnaround with a dedicated team or expert |

| Accuracy | Prone to errors if you lack bookkeeping knowledge | High accuracy with expert handling and review |

| Use of Accounting Software | May struggle with setup or advanced features | Fully set up and optimized for tools like QuickBooks, Xero, FreshBooks |

| Tax Readiness | Risk of missed deductions or filing errors | Ensures books are compliant and ready for tax season |

| Error Correction | You may not notice or know how to fix past mistakes | Professional’s review, adjust, and fix old errors (e.g., misclassifications) |

| Long-Term Impact | May need to redo work if errors are found later | Provides a solid foundation for financial planning and decision-making |

However, DIY catch-up bookkeeping may be cost-effective, but due to lacks of expert knowledge, it increases the risk of receiving penalties or fines from the IRS due to errors or misinterpretation.

How Much Does Catch-Up Bookkeeping Cost?

Typically, the cost of a catch-up bookkeeping isn’t one-size-fits-all, it depends on several factors. The price of a bookkeeping is affected by the period you need to catch up on, number of transactions and the condition of your existing records. Professional bookkeepers usually charge around $25 per hour.

Eventually, spending on catch-up bookkeeping is not just about getting your numbers in order—it’s about avoiding penalties, getting clarity on your business for better decision-making

When Should I Hire a Professional for Catchup Bookkeeping?

Falling behind on your books can be fine until it’s the tax season. Hiring a professional bookkeeper isn’t just helpful, it’s essential for keeping your business compliant and financially healthy.

Here are specific situations when you should hire a bookkeeper:

- It has been more than 3 months since your last update on books

- It’s time to file taxes or apply for a loan

- There is high volume or complexity in your transactions

- Inconsistencies or errors in your books have caught your attention

- Your books are taking up more of your time than your business

If any of these situations arise, hiring a professional bookkeeper isn’t just a solution it’s a smart investment in your business’s future.

Frequently Asked Questions (FAQs)

What is the difference between catch-up bookkeeping and clean-up bookkeeping?

Catch-up bookkeeping, as name suggests, is a process to records missed financial transactions that has accumulated for a past period. On the other hand, Clean-up bookkeeping, involves fixing errors, inconsistencies, or disorganized records in books that were maintained

How many months of bookkeeping can I fall behind before I need catch-up services?

Generally, if you are behind by 3 months or more, it’s a good time to consider the service. However, some companies seek service after 6–12 months of delay, especially during tax season or audits.

Can I do catch-up bookkeeping on my own using QuickBooks or Xero?

Yes, you can with the help of tools like QuickBooks or Xero, which are popular accounting software in the US. However, if your transaction volume is high or complex, there’s a greater risk of errors, missed tax deductions, or incorrect reconciliations without professional accounting knowledge

Will catch-up bookkeeping help me avoid tax penalties?

Yes, regular catch-up bookkeeping ensures your financials are accurate and tax-ready, helping you avoid late filing fees, interest, and IRS penalties

What documents do I need to start catch-up bookkeeping?

Typically, you’ll need to provide:

1. Bank and credit card statements (including statements for any US-based accounts)

2. Receipts and invoices

3. Payroll reports (including W-2s or 1099s where applicable)

4. Loan or debt records

5. Previous accounting reports or spreadsheets (if available)

The more complete your documents, the faster and smoother the process will be.

Is it worth hiring a professional if I’m only 3 months behind?

Yes, even short delays can turn into bigger issues, especially if you’re nearing tax deadlines or lack the time or expertise to do it correctly. A professional can clean up your books efficiently—saving you time and stress

What is catch-up in accounting?

Accountants use the catch-up approach to reconcile and update overdue financial records, utilizing methods such as data collection, reconciliation of account, correction of errors, adjusting entries, and detailed documentation

What is the difference between bookkeeping and catch-up bookkeeping?

Bookkeeping is the process of maintaining all your business’s financial records on a regular basis whereas catch-up bookkeeping occurs mainly after a few gaps of a few months or a year to get back on the books

Conclusion

Falling behind on your books doesn’t mean you’ve failed in your business, it means you’re busy in establishing your business. But staying behind and facing legal issues? That’s where problems begin. Catch-up bookkeeping is a decisive step toward financial clarity, tax compliance, and informed decision-making and much more than a clean-up service. Whether you’re a few months or a year behind, taking action now can save you time, stress, and money later. So, don’t let outdated books hold your business back. Get caught up, stay compliant, and move your company forward with confidence.