Budget overruns don’t just harm your margins; they quietly ruin your profitability, damage customer relationships, and hinder your contractor growth. “We’ll fix it later” is no longer an option in today’s competitive construction market where every change order, material increase, and delay impact your bottom line.

This is where project accounting comes in. It improves clarity and transparency by recording costs in real time, allocating every penny to specific projects, and providing transparent information about personnel, materials, administrative expenses, and project progress. This way, you don’t have to wait until the project is finished to discover cost overruns; instead, you can identify problems early in the project, develop action plans, and ensure cash flow.

In this blog, we will look at how construction-focused project accounting may help contractors avoid budget overruns, close projects more correctly, and create a healthier, more dependable business all without having to become a full-time accountant.

What Is Construction Project Accounting?

Construction project accounting is a specific method of handling your finances in which each task is handled as its own mini-business. Instead of focusing on your company’s overall profit and loss, you track income, and profit for each particular project from beginning to ending.

For contractors, this involves delegating each work hour, material purchase, subcontractor bill, equipment charge, and change request to a particular job. This allows you to monitor in real time whether a project is on budget, where costs are slipping, and how much profit you will make once the job is completed.

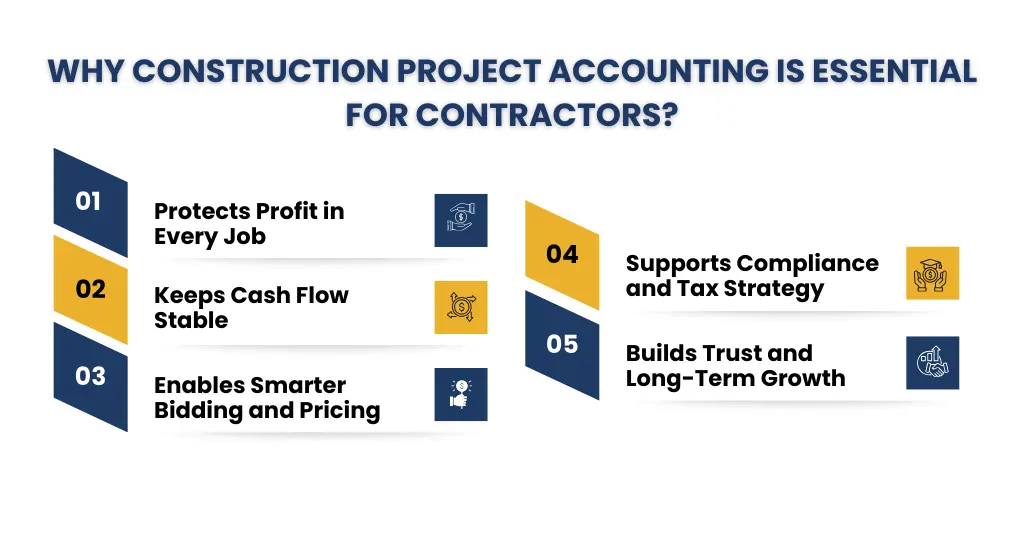

Why Construction Project Accounting Is Essential for Contractors?

Construction project accounting is essential because it is the only method for contractors to determine whether contracts are actually profitable, not just busy. It transforms guesswork into statistics, allowing you to manage costs, preserve cash flow, and develop with confidence.

Protects Profit on Every Job:

Labor, supplies, equipment, and overhead are tracked by project accounting, allowing you to see exactly which jobs are profitable or losing money. Variance analysis (budget vs. actual) allows you to identify overruns early and take remedial action before margins vanish.

Keeps Cash Flow Stable:

Progress billing, retainage tracking, and accurate invoicing let you bill on time and collect what you owe. Monitoring payables and receivables by task allows you to avoid cash flow problems even when a project appears profitable on paper.

Enables Smarter Bidding and Pricing:

Job-level history shows you the actual prices of previous projects, allowing you to appropriately begin future work rather than undercutting yourself. Post-project analysis identifies the most profitable project types, clients, or scopes, influencing your sales and bidding approach.

Supports Compliance and Tax Strategy:

Handles construction-specific requirements such as revenue recognition methods (% of completion, finished contract) and the proper treatment of work in progress. Clean, project-based records make tax filing, auditing, and lender/bonding requirements simpler and less dangerous.

Builds Trust and Long-Term Growth:

Clear, precise billing and backup documentation help to resolve conflicts and enhance client relationships. Reliable financial reporting offers you and your lenders the confidence to embark on larger, more complex projects without losing control.

Construction Accounting vs Project Accounting

| Aspect | Construction Accounting | Project Accounting (in Construction) |

| Primary focus | Overall financial health of the construction company | Financial performance of each individual job or contract |

| Scope | Company-wide (all projects, overhead, assets, liabilities, taxes) | Single project (revenues, direct costs, margin, cash flow) |

| Key activities | Financial reporting, WIP schedules, retainage tracking, tax compliance | Job costing, budget vs. actual tracking, forecasting, variance review |

| Time horizon | Ongoing, across fiscal years | From start of project to closeout |

| Typical outputs | Balance sheet, income statement, cash flow statement, WIP report | Job cost reports, cost-to-complete, project margin and KPI reports. |

Accounting Programs for Construction Companies

- QuickBooks (with Job Costing): QuickBooks is a popular choice among small & medium-sized contractors because it makes it pretty easy to handle invoicing, payroll, and basic work costing. You can essentially treat each project like a customer and track labor, materials & subs connected to it – all with the ability to generate job-cost and profit reports.

- Sage Construction Solutions: Sage 100 Contractor and Sage 300 CRE are the go-to solutions for the construction and real estate industries. These systems combine core accounting functions with comprehensive job costing – meaning you get reporting on work-in-progress, progress billing, subcontract management, and the powerful reports lenders and bonding organizations demand.

- Xero with Construction Add-ons: Xero is great for contractors who need flexibility and loads of integrations – it’s cloud-based, so you can access it from anywhere. When you add some construction apps (think work costing, timesheets, project management) to the mix, Xero gives you real-time insight into project margins and your cash flow.

- Construction ERPs (CMiC, Jonas, Viewpoint, and others): If you’re a bigger contractor or looking to scale, you’ll probably end up switching to a full construction ERP like CMiC, Jonas or Viewpoint. These systems bring all the key components – like accounting, project management, payroll, equipment & field operations – together into one platform. That means your finance & site teams can share the same data, operate as one seamless unit.

Key Principles of Construction Cost Accounting

Here are the key construction cost accounting principles explained:

Job Costing as the Core:

Construction cost accounting in the United States is based on job costing, in which each cost is assigned to a specific project, phase, or cost code rather than being categorized as a generic expense. This allows contractors to see genuine profitability by task and enables extensive reporting for lenders, bonding businesses, and tax purposes.

Direct vs. Indirect Costs:

Costs are divided into direct costs (people, materials, subcontractors, and equipment) that can be traced back to a specific task and indirect costs (overhead, office wages, insurance, and rent) that must be spread across multiple projects. US regulations demand that overhead be handled in a consistent manner so that no project is over- or under-loaded with shared costs.

Revenue Recognition (US GAAP & Tax Rules):

Under US GAAP, construction companies often recognize revenue using accrual-based methodologies like percentage-of-completion (POC), which match income to work completed over time. Smaller contractors (those with typical gross revenues of $25 million or less) may be able to use the simpler cash method for tax reasons, however bigger contractors must normally use accrual/POC or other permitted long-term contract techniques.

According to IRS regulations, FASB’s ASC 606 framework, larger construction companies are generally required to recognize revenue using percentage-of-completion methods, while qualifying small contractors may elect the cash method for tax reporting.

Matching Costs to Revenue:

The matching principle requires that project costs be recognized in the same period as the corresponding project revenue. In reality, this means tracking and recording labor, material, subcontractor, and equipment expenses as work advances, ensuring that WIP (work in progress) and job profitability are accurate at each reporting date.

Work-in-Progress (WIP) Tracking:

WIP schedules are a critical component of US construction cost accounting, displaying contract value, costs to date, billings to date, and over/under-billing for individual jobs. These reports help contractors determine if they are ahead or behind on revenue recognition and cash, and they are frequently needed by banks and sureties.

Strong Budgeting and Cost Control:

Setting comprehensive budgets by job and cost code, followed by tracking budget vs. reality throughout the project, is an example of effective cost accounting. Regular variance analysis enables US contractors to identify overruns early, update projections, and take corrective action before margins diminish.

The Role of Job Costing in Construction Project Accounting

Job Costing – The Key to Construction Project Accounting

Job costing is pretty much essential to construction project accounting. It works by attaching every single dollar spent to a very specific task or job. When you allocate personnel, supplies, subcontractors, equipment and all the overhead to each project, it transforms a construction job from a wild guess into a clear profit and loss statement.

Getting to the Bottom of Project Costs: By making sure that every last cost, direct or indirect is assigned to the right project or phase, job costing lets you keep a super close eye on exactly where all your money is going.

Protecting Your Margin: Because job costing gives you the actual cost of a job after it’s all over, it makes a great feedback loop for future estimates and bids. You can compare cost to estimate, tweak your pricing, and focus on the jobs that give you the highest margins.

Keeping Your Project on Track: Job costing gives you a real time budget vs actual data for each project, so you can get a sense of cost to complete and profit at any given time. When your expenses start running ahead of your projections project managers can tweak the scope, negotiate some change orders, or reallocate resources before it’s too late to correct the problem.

Tying Costs to Revenues: And for contractors who use accrual methods like percentage of completion, job costing gives them the exact numbers they need to figure out how much revenue they can recognize and update their WIP plans. By matching specific job expenses to the revenue you’ve actually earned, you can make sure your financial statements are solid and give investors, lenders and sureties a clear picture of project health.

Understanding Construction Work-in-Progress (WIP)

Construction work-in-progress (WIP) is a rolling total of how much work has been completed on your open jobs, how much it has really cost you thus far, and how much money you have generated but have not yet recognized. It serves as a link between the field and your finances, displaying the dollar value of each ongoing project rather than its percentage completion.

In accounting, work in progress (WIP) represents the cumulative job expenses and earned revenue on projects that have begun but have not yet been completed, and it is often summarized in a WIP timeline. This schedule shows each contract, its value, costs to date, billings to date, expected costs to completion, and if you were overbilled or underbilled for that job.

Understanding work in progress (WIP) is crucial for contractors because it drives accurate revenue recognition (particularly using approaches such as percentage-of-completion), identifies problem tasks early, and is sometimes required by banks and sureties when applying for financing or bonding. A well-maintained WIP report allows you to determine which projects are silently losing money, which are supporting others by overbilling, and whether your stated profit matches reality on the ground.

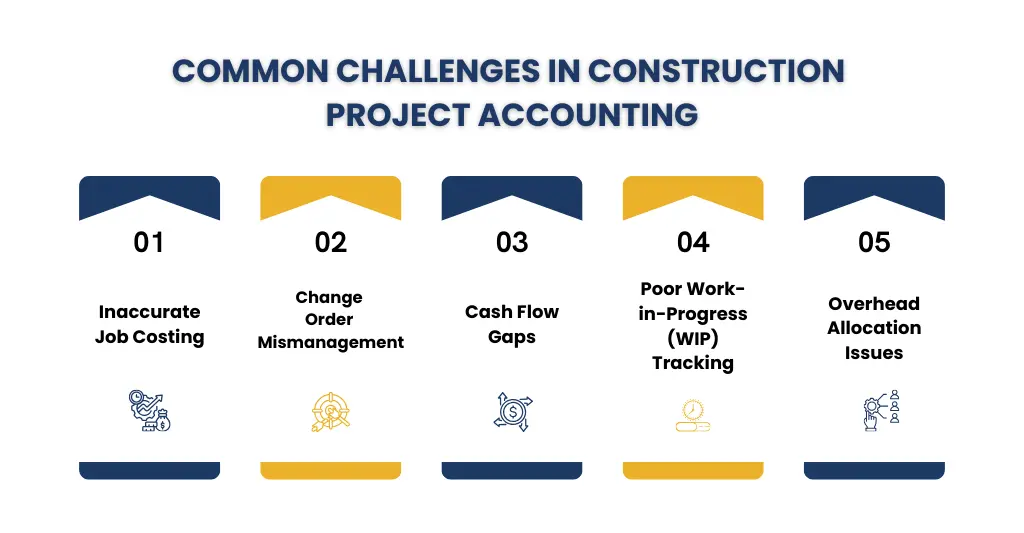

Common Challenges in Construction Project Accounting

Construction accounting is not the same as normal company accounting. Every task is unique, schedules vary, and expenses rarely remain constant. Without effective financial controls, minor errors can swiftly turn into significant profit leaks.

Here are some of the most common challenges contractors face:

Inaccurate Job Costing: If labor, material, and subcontractor expenses are not properly tracked by job and cost code, it is practically hard to determine whether a project is profitable.

Change Order Mismanagement: Unapproved or inadequately recorded modification orders can result in unpaid work and declining profitability.

Cash Flow Gaps: Progress billing delays, retainage, and late payments can all put an impact on cash flow, even if projects appear successful on paper.

Poor Work-in-Progress (WIP) Tracking: Without correct WIP reporting, revenue recognition is unreliable, resulting in misleading financial statements.

Overhead Allocation Issues: Failure to correctly allocate equipment, insurance, and indirect costs can make successful jobs appear unprofitable, and vice versa.

Keep Your Construction Project Accounting Under Control

Profit in construction is not made at the end of the project; rather, it is protected every day on the job. When construction project accounting is not closely controlled, minor mistakes can quickly escalate into costly concerns. Delayed change orders, untracked labor hours, faulty work costing, or missed subcontractor bills can all eat into your profits before you know it.

Keeping your construction project accounting under control means having real-time visibility into:

- Job costing and cost codes

- Labor, materials, and equipment tracking

- Change order management

- Work-in-progress (WIP) reporting

- Progress billing and retainage

- Cash flow forecasting

- Compliance with U.S. GAAP and IRS requirements

Contractors in the United States work in a high-risk, high-cash flow environment. Between progress payments, retainage, subcontractor payments, and fluctuating material costs, a single accounting miscalculation can cause payroll delays or strain on vendor relationships.

Struggling With Construction Project Accounting Across Your US? Corient helps US contractors track every dollar, stay IRS-compliant, and close projects on budget — without the accounting headache.

FAQs: Frequently Asked Questions

What type of accounting is used in construction?

Construction accounting is a project-based accounting approach that records income and expenses for particular jobs.

In the United States, contractors commonly use:

1. Percentage of Completion Method (PCM): Revenue is recorded based on project progress.

2. Completed Contract Method (CCM) – Revenue is recorded once the project is completed.

This strategy also includes job costing, work-in-process reporting, and progress billing to assist contractors in precisely managing profitability and cash flow.

How do you record construction accounting?

Construction accounting is organized by project (job-based accounting), rather than by month. Here’s how it’s usually done in the United States:

Assign Cost codes for labor, materials, equipment, and subcontractors

Track spending per project using job costing.

Record revenue using either the Percentage of Completion (PCM) or the Completed Contract Method (CCM).

Maintain work-in-process (WIP) reports to track project performance.

Manage progress billing and retention independently.

This strategy assures that contractors can track project profitability, manage expenses, and provide accurate financial reporting throughout the project’s lifecycle.

How does job costing improve construction profitability?

Job costing increases construction profitability by recording all expenses associated with each individual project, including personnel, materials, equipment, and subcontractors.

By assigning costs to specific jobs and cost codes, contractors can:

Identify cost overruns early

Compare actual costs vs. budget

Control labor and material waste

Improve future bidding accuracy

Protect profit margins

When work costing is done effectively, contractors receive real-time visibility into where money is being spent, allowing them to make faster decisions and prevent minor errors from escalating into big losses.

Is there a difference between work-in-process and work-in-progress in accounting?

The finest construction accounting software should include job costing, work-in-process reporting, progress billing, and cost tracking.

These are the most significant options:

QuickBooks (Online/Desktop) is best suited for small to mid-sized contractors; add-ons enable task costing.

Sage 100 Contractor – Designed exclusively for construction, with robust payroll and project tracking.

Viewpoint Vista – Ideal for large contractors who require full ERP functionality.

Foundation Software is a job cost-focused system built specifically for contractors.

Your company’s size, project complexity, and reporting requirements all influence the best option.

Conclusion

Construction is complex, and your accounting should deliver clarity rather than uncertainty. Even profitable projects can soon become financial stress if job costs, work in progress reporting, progress billing, and revenue recognition are not properly tracked. The idea is to have accurate, real-time visibility into each project so you can control costs, protect margins, and make sound decisions.

That’s where expert Construction Project Accounting Services can help. Contractors can speed up financial procedures, stay compliant with US rules, and focus on project delivery rather than chasing figures if they have the necessary skills and technologies. When your accounting is structured and proactive, your construction company does more than just build projects; it also produces long-term profits.