Managing properties without sufficient recordkeeping is like trying to build a project without the blueprint plan. When your income, expenses, and owner funds are all carefully tracked, you can answer challenging questions, prevent unexpected cash crunches, and make better decisions regarding each unit you manage.

You’ll discover the key financial practices that set successful property managers apart—like properly reconciling accounts, handling trust money the right way, and tracking performance at the property level.

1. Use Separate Accounts to Simplify Property Management Bookkeeping

Maintaining clear financial separation is one of the most critical bookkeeping elements in property management, but it is also one of the most usually missed areas.

Why do separate accounts matter?

Separate accounts are necessary because if you mix rental income, owner funds, and business operational expenses in a single account it will create confusion for yourself. It also increases the chances of errors, and makes compliance more difficult. Whereas, maintaining separate accounts will keep record error less, faster reconciliations, and better reporting to landlords and tax authorities.

Key accounts every property manager should maintain:

Operating account – Used for day-to-day business expenses such as marketing, admin costs, and management fees.

Client (trust) account – Holds rent collected on behalf of landlords and must never be mixed with business funds.

Security deposit account – Keeps tenant deposits ring-fenced, making it easier to comply with deposit protection rules.

2. Build a Clear Chart of Accounts

A proper well-structured chart of accounts is the backbone of accurate property management bookkeeping. Otherwise, without tracking income, expenses, and owner balances will become messy. Especially if you are managing multiple properties.

What a chart of accounts does?

The chart of accounts is a classified list of all financial transactions in your company. For property managers, it ensures that every pound is accurately recorded and linked to the correct property, landlord, or tenant.

Key categories to include:

Rental income – Rent received, late fees, and other tenant charges

Management fees – Fees earned for managing properties

Property expenses – Repairs, maintenance, utilities, insurance, and council tax (if applicable)

Owner-related accounts – Owner contributions, withdrawals, and reserves

Tenant deposits – Security deposits and refunds

Operating expenses – Office costs, software, marketing, and professional fees.

3. Choose the Right Accounting Method

Choosing the appropriate accounting method is an important decision in property management bookkeeping. It influences how and when income and spending are recorded, which has a direct impact on financial reporting and tax calculations.

The two main accounting methods:

Cash basis accounting: Income is recorded when rent is received, whereas expenses are recorded when they are paid. This strategy is easy and effective for modest property portfolios or individual landlords who conduct routine transactions.

Accrual accounting: Income and costs are recorded whenever they are earned or incurred, regardless of when the money changes hands. This strategy provides a more realistic picture of financial success and is widely employed by rising property management companies.

How to choose the right method?

- If you manage a few properties with basic cash flow, the cash basis can be sufficient.

- If you deal with several properties, landlords, or long-term contracts, accrual accounting provides superior insight and control.

- Consider tax and reporting regulations, as certain organizations may need to employ accrual accounting.

- Considering future growth changing approaches later can be complex.

4. Use Double-Entry in Property Management Bookkeeping

Double-entry bookkeeping is more than just an accounting requirement; it ensures accuracy, transparency, and control in property management. When dealing with rent, deposits, and landlord finances, doing this properly is critical.

What does double-entry bookkeeping mean?

Every financial transaction is recorded twice: as a debit in one account and a credit in the other. This assures that the books are constantly balanced and that every financial transaction can be traced.

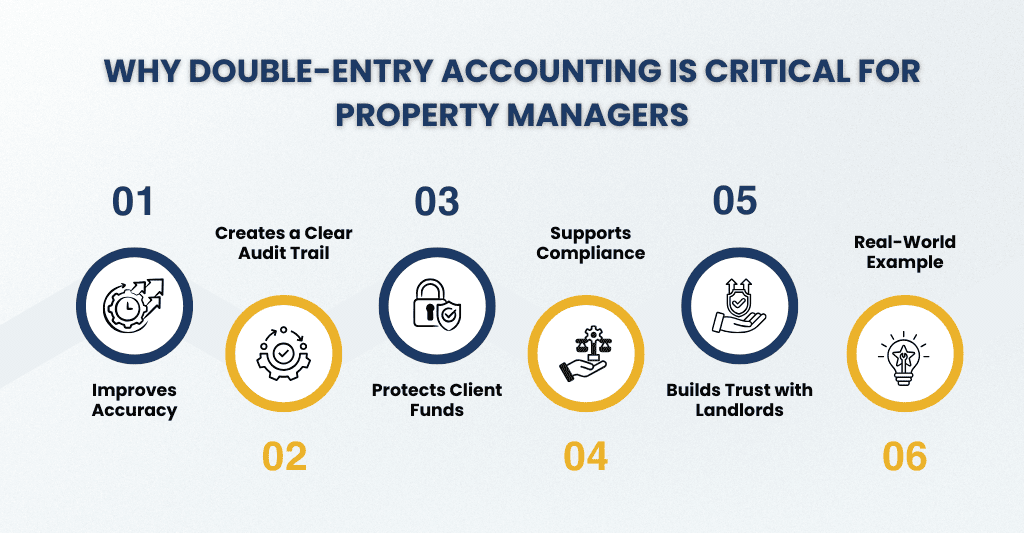

Why is it critical for property managers?

Improves Accuracy: Errors are easier to detect when debits and credits are balanced.

Creates a clear audit trail: Every transaction can be traced back to its source.

Protects client fund: Client cash is kept safe by ensuring rent and deposits are accurately allocated and not mixed with business income.

Supports compliance: Necessary for audits, tax filings, and regulatory reviews.

Builds trust with landlords: Transparent records make reporting clearer and more professional, which increases trust with landlords.

Real-world example: When rent is received, double-entry accounting is used to record the cash in the client account as well as the landlord’s liability. This avoids rent from being incorrectly classified as business income.

5. Track Rent Payments Consistently

Rent tracking consistency is essential for accurate property management bookkeeping. Incomplete or inaccurate rent records cause cash flow concerns, landlord disputes, and time-consuming fixes.

Why does consistent tracking matter?

- Ensures that rent payments match bank deposits.

- Helps locate late or missed payments promptly.

- Ensures correct landlord statements and reporting.

- It prevents income from being inflated or missing.

- Makes reconciliations faster and less stressful.

What to track for every rent payment?

- Tenant name and property address

- Rent period covered (week or month)

- Amount due vs. amount received

- Payment date and method

- Any arrears, partial payments, or adjustments

6. Record Every Expense Promptly

Recording expenses as soon as they occur is a simple practice that has a significant impact on property management bookkeeping. Delays can result in missed receipts, incorrect reporting, and unnecessary confusion later on.

Why prompt expense recording matter?

- Keeps cash flow and profitability accurate.

- Keeps expenses from being forgotten or repeated.

- Makes landlord statements more reliable.

- Simplifies month-end and year-end closure.

- Ensures proper tax and compliance reporting

Expenses property managers should track:

- Repair and maintenance costs

- Utilities and council tax (where applicable).

- Invoices issued by contractors and vendors

- Fees for letting and advertising

- Insurance, software, and administrative expenses.

7. Manage Security Deposits Correctly

Security deposits are not considered corporate income; they are tenant monies held in trust. Managing them effectively is an important aspect of property management bookkeeping, and errors can lead to compliance concerns.

Why correct deposit management matters?

- Protects tenant cash from misuse

- Helps meet legal and regulatory obligations.

- Prevents disagreements at the end of the tenancy.

- Maintains clear and accurate records for landlords and tenants.

Key bookkeeping rules for security deposits:

- Keep deposits separate: Always keep deposits in a dedicated deposit or trust account, not in your operational account.

- Record deposits as liabilities: Deposits belong to the tenant until lawfully released; hence, they should not be considered as income.

- Track per property and tenant: Each deposit should be properly linked with the particular property and tenant.

- Document deductions clearly: Any deductions for damage or overdue rent must be justified by reliable documents.

8. Reconcile Accounts Monthly

Monthly reconciliation is one of the most important things that needs to be followed for property management bookkeeping. It ensures that your records match with the actual reality and allows you to identify errors before they become larger problems.

What does reconciliation mean?

Reconciliation is the process of checking your bookkeeping records against bank statements, deposit accounts, and client or trust accounts to ensure that all transactions are correct and complete.

Why does monthly reconciliation matter?

- Identifies missing, duplicated, or inaccurate entries.

- Checks rent and spending data against bank activity.

- Detects fraud or illegal transactions earlier.

- Keeps landlord statements accurate and reliable.

- Makes year-end reporting much less burdensome.

9. Review Your Financial Reports Regularly

Regularly reviewing your financial reports transforms property management bookkeeping services data into actionable insights. In property management, this allows you to maintain control over cash flow, identify problems early, and make smarter decisions for landlords and your company.

Why does regular review matter?

- Highlights unpaid rent, growing costs, or cash flow imbalances.

- Ensures that reports shared with landlords are correct and thorough.

- Detects problems before they impact tax filings or audits.

- Encourages better budgeting and forecasting.

- Increases your confidence in financial management.

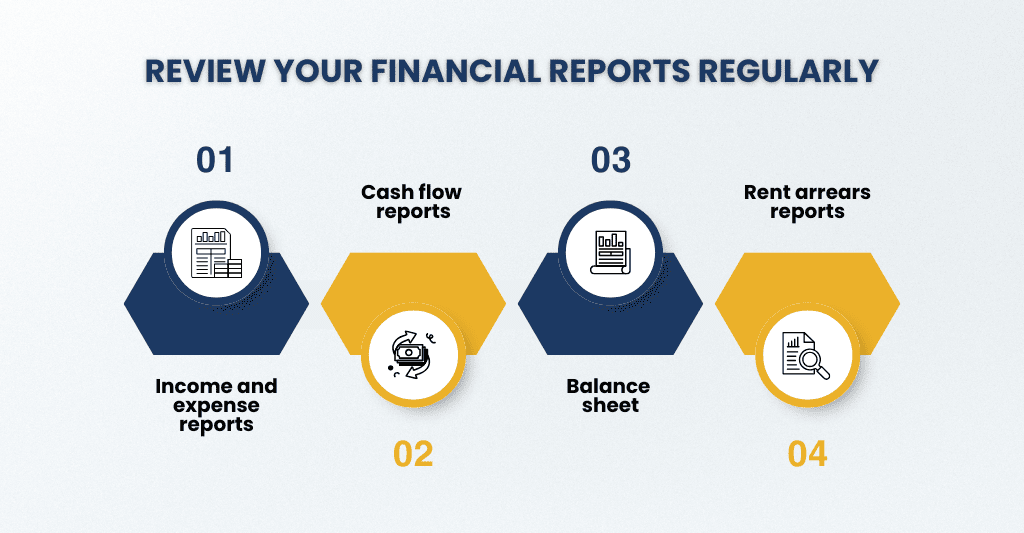

Key reports to review

- Income and expense reports – Check rental income against property-related costs

- Cash flow reports – Ensure sufficient funds for upcoming expenses and distributions

- Balance sheet – Review liabilities such as deposits and owner balances

- Rent arrears reports – Monitor late or outstanding payments

How often should you review them?

- Monthly for internal management and reconciliations

- Quarterly for trend analysis and planning

- Year-end for tax preparation and compliance

10. Use the Right Bookkeeping Tools and Software

Using the right property management bookkeeping software speeds up and improves the accuracy of property management. Good tools automate rent tracking, expense recording, and reconciliation, reducing manual errors.

Choose software that allows for property-level reporting, separates client and deposit funds, and interfaces with bank feeds. The right approach saves time, improves accuracy, and keeps your bookkeeping in order as your portfolio grows.

Take charge of your property management finances today! Learn the essential bookkeeping basics every manager must know to keep your business running smoothly. Click here to master your financial management now!

FAQs: Frequently Asked Questions

When should property management seek professional bookkeeping help?

Professional assistance is beneficial when managing several properties, handling client funds, or devoting too much time to finances. Property management accountants and bookkeeping services help to ensure accuracy, compliance, and consistency as portfolios grow.

Should property managers maintain separate accounts for each property?

Yes. Keeping separate or properly maintained accounts makes it easier to handle rent, bills, and deposits. It increases transparency, streamlines reconciliations, and prevents the mixing of corporate and customer cash.

Why is precise bookkeeping essential in property management?

Accurate bookkeeping allows property managers to accurately track rent, costs, and deposits. It reduces errors, promotes compliance, and offers clear, dependable reporting for landlords and tenants.

What are the three types of bookkeeping?

Single-entry

Double-entry

Virtual bookkeeping.

What is the most challenging part of property management?

Common Challenges—and How to Tackle Them

Tenant Satisfaction: Address issues with clear communication.

Efficient Repairs: Stay organized to avoid getting overwhelmed.

To-Do List Management: Prioritize and delegate tasks.

Housing Law Compliance: Stay updated on legal requirements.

Filling Units: Focus on quality tenants, not just quantity.”

Conclusion:

Strong bookkeeping is at the heart of a smooth and stress free property management experience. Let’s get real, getting the little things right like keeping accounts separate and making sure you’re keeping track of that rent money on a regular basis, its the key to avoiding a world of trouble, keeping things transparent and making sure the landlord trusts you to get the job done. While it sounds like a pain, doing some of these small things day in day out makes all the difference when it comes to accuracy and following the rules.

A lot of property managers will tell you that having a good property management bookkeeping accountant in their corner makes a huge difference. No more stress and hassle trying to keep tabs on the financials, they’ll leave that to the experts who can give you peace of mind that the books are accurate, deposits are done right and when you need a report, it’ll be ready for you. Which lets you get back to what matters – actually managing properties rather than getting frustrated in the numbers game.