Taxation can be a real burden for lots of people, from individuals to businesses, and the thing is, many of us are probably leaving money on the table because we’re not taking advantage of all the tax deductions that are available to us – it’s a big reason why thinking ahead and getting a handle on your tax strategies situation before the year is up can make all the difference

With the constant changing of tax laws, new limits on deductions, and shifting tax policies, it’s getting harder and harder for people to stay on top of it all. As a result, many people end up missing out on big savings by doing the bare minimum with their taxes, right up until the last minute before the deadline.

But the thing is, with a bit of common sense, keeping track of your finances properly, and keeping your records ship shape, you can significantly reduce your tax bill without breaking any rules.

In this blog, we’re going to reveal 15 practical tax strategies that can help both individuals and businesses squeeze every last penny out of their deductions, make the most of their money and make better decisions when it comes to filing their tax return.

What is Tax strategy?

An effective tax strategy is the way an individual or company goes about legally slashing their tax bill, all while still respecting the tax laws of course. Tax strategies involve juggling income and expenses, making smart investments, making financial decisions and making the most of the tax breaks that are on the table – tax deductions, tax credits and tax allowances all count.

Rather than waiting until the end of the tax year to get everything sorted, a solid tax strategy involves planning ahead all year round, so taxpayers can avoid shelling out too much in taxes, breathe a bit easier on the cash flow front and steer clear of any penalties.

Companies will use all sorts of tactics to shave off as much of their overall tax bill as possible, from claiming all the tax deductions they’re eligible for, to timing when they bring in income and pay out expenses, to putting money into retirement plans and claiming tax credits wherever they can.

Why Tax Strategy Matters More Than Ever?

Every year, the complexity of tax rules, compliance procedures, and reporting duties grows. Governments are expanding their surveillance of organizations and individuals, while digital tax systems and tougher reporting requirements leave little space for error.

Many taxpayers overpay, miss out on qualifying tax deductions, or face penalties due to poor planning. The One Big Beautiful Bill Act has also introduced key changes for 2025 and 2026 — including increased standard deductions and modified depreciation rules — making proactive tax saving strategies more important than ever.

A proper planned tax strategy will help you:

- Use available deductions and credits to reduce your overall tax income.

- To improve cash flow, schedule taxes ahead of time instead of reacting at the last minute.

- Stay compliant with new tax requirements to avoid penalties.

- Make more informed financial decisions concerning investments, spending, and business growth.

If you’re not sure where to start, E2E Accounting’s Tax Preparation Services can help you put a plan in place from the ground up.

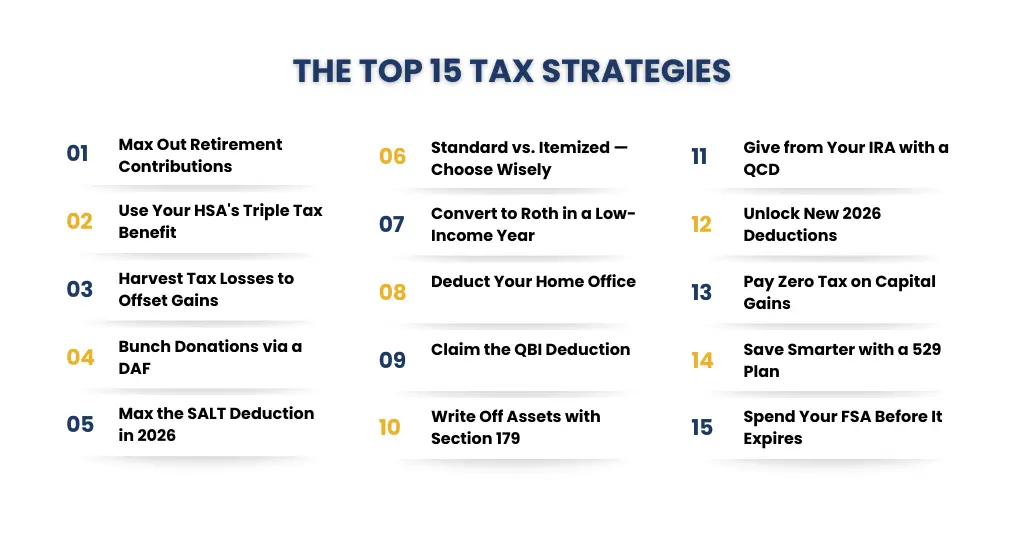

The Top 15 Tax Strategies to Know

Strategy #1: Make the Most of Your Retirement Account Contributions

One of the most reliable tax strategies is contributing to a retirement plan like a 401(k) or traditional IRA,you could slash your taxable income and put a bit more money towards your golden years in the long run. Plus, these contributions usually qualify for some serious tax deductions – so you’ll pay less now and have more set aside for later on.

Strategy #2: Tap Into The Triple Tax Advantage of a Health Savings Account

HSAs have three awesome tax benefits: the cash you put in is tax deductible, the money it grows is tax-free, and then – if you use it for medical expenses – the withdrawals are tax-free. This makes it one of the smartest tax-savvy moves you can make.

Strategy #3: Use Tax Loss Harvesting to Even Out Your Investments

Tax-loss harvesting lets you sell some of the investments that haven’t panned out so you can offset the gains on the investments that are performing well. This helps keep your overall investment income as low as possible.

Strategy #4: Max Out Your Charitable Giving With a Donor-Advised Fund

Rather than giving little here and there, some smart folks bunch up their donations into one year using a donor-advised fund. This lets you sock away a big chunk of cash and boost your tax savings at the same time.

Strategy #5: Get The Most Out of The SALT Deduction In 2026

The State and Local Tax deduction lets you deduct a certain amount of state and local taxes. If you plan ahead with your property and state income taxes, an often overlooked element of effective tax strategies.

Strategy #6: Standard Deductions vs Itemized Deductions – Which One Pans Out For You?

Taxpayers have a choice to make each year: do you take the standard deduction or try to itemize – and see which one leaves you with more in your pocket. If you have expenses like mortgage interest, charitable donations or medical fees, you might be better off itemizing.

Strategy #7: Do A Roth Conversion When Your Income is Low

If you convert a traditional IRA to a Roth in a year when your income is relatively low, you’ll pay less in taxes on the conversion – and Since future withdrawals from a Roth are tax-free, this is one of the smarter long-term tax strategies for retirement planning.

Strategy #8: Deduct Home Office Expenses If You Work From Home

If you work from home and use a dedicated space for business, you might be able to deduct a percentage of your rent, utilities and internet costs – that’s a nice little savings right there.

Strategy #9: Take Advantage of The Qualified Business Income Deduction

Business owners with qualifying income may be eligible to deduct up to 20% of it under the QBI deduction. This is one of the most impactful tax strategies available for small business owners and freelancers.

Strategy #10: Make the Most of Bonus Depreciation and Section 179

Businesses can write off a big chunk of the cost of new equipment or tech purchases in the year they buy it, using bonus depreciation or the Section 179 deduction – this can be a real game-changer.Under rules updated by the One Big Beautiful Bill Act, these provisions remain a powerful planning tool for 2026.

Learn more about how this applies to your business through E2E Accounting’s Business Income Tax services.

Strategy #11: Use a Qualified Charitable Distribution to Give to Charity & Save on Taxes

If you’re 70 1/2 or older, you can donate directly from your IRA to a qualifying charity – this lets you reduce taxable income while still supporting a good cause.

Strategy #12: Take Advantage of the New 2026 Deductions

New tax laws and deductions implemented in 2026 may provide further options for tax savings. Reviewing current rules with a tax professional ensures that you take full advantage of all applicable allowances.

Strategy #13: Harvest Capital Gains at the 0% Rate

Some taxpayers in lower tax bands may be eligible for 0% long-term capital gains taxes. Selling appreciated investments strategically during these times allows you to lock in profits without incurring further tax liabilities, a well-timed move that’s central to smart tax strategies for investors.

Strategy #14: Contribute to a 529 College Savings Plan

Some taxpayers in lower tax bands may be eligible for 0% long-term capital gains taxes. Selling appreciated investments strategically during these times allows you to lock in profits without incurring further tax liabilities.

Strategy #15: Use Flexible Spending Accounts (FSA) Before Year-End

Flexible Spending Accounts enable employees to save pre-tax income for medical or dependent care needs. Because most FSAs have a “use-it-or-lose-it” policy, spending these funds before year-end helps to prevent losing the benefit. This is one of the simplest tax saving strategies available through most employer benefit plans.

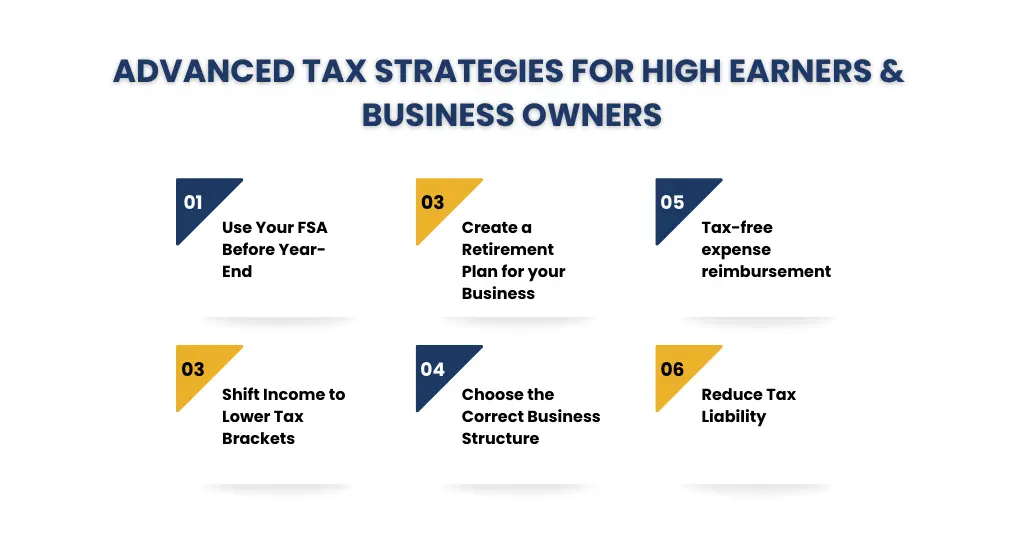

Bonus Strategies — For High Earners & Business Owners

Make the Most of Your FSA Before Year-End:

Flexible Spending Accounts give all employees a chance to stash some of their income before taxes for things like doctor visits and childcare. But if you don’t use up all the funds by the end of the year, you’re basically throwing those pre-tax savings down the drain. To make the most of your FSA and keep that pre-tax benefit, try to spend down your contributions during the calendar year to avoid losing it.

Shift Some of Your Income to Family Members in Lower Tax Brackets:

Business owners can use this trick to offset some of the money they have to pay in taxes on their business’s profits. One way to do this is by paying dividends or salaries to family members in lower tax brackets (that’s your spouse, kids, etc.).

Set Up a Business Retirement Plan & Help Your Employees Out:

Setting up a retirement plan – like a SEP-IRA, Solo 401(k) or defined benefit plan – also lets you take even more tax-deductible contributions for yourself. And this benefits your employees too by giving them a retirement plan at work.E2E Accounting’s Financial Planning and Advisory Services can help structure the right plan for your situation.

Pick a Business Structure That’ll Save You Some Cash:

Choosing the right business type – whether it’s a S-Corp, LLC or Partnership – can make a huge difference when it comes to how your business profits are taxed. This structural decision is one of the most impactful long-term tax strategies a business owner can make.

Tax-free expense reimbursement:

It is possible to structure an Accountable Plan to provide business owners and employees with reimbursement for work related expenses such as vehicle usage, home office expenses or equipment purchases tax-free. This is a cornerstone of effective tax strategies for businesses of all sizes.

Reduce Tax Liability:

Optimally timing the income and the expense of the business can allow for deferring income and/or accelerating the expenses accrued toward the end of the year. This will reduce the current taxable income of the business and therefore provide the opportunity to better manage cash flow.

These solutions can significantly improve overall tax efficiency and long-term financial planning for high-income individuals and developing businesses.

See also: Don’t Wait Until April: A Business Owner’s Guide to Year-End Tax Deductions — an in-depth look at year-end planning on the E2E Accounting blog.

Common Tax Strategy Deduction Mistakes to Avoid

- Not maintaining proper records or receipts for deductible expenses.

- Forgetting to track tiny expenses that accumulate throughout the year

- Claiming deductions without accompanying paperwork.

- Combining personal and commercial financial transactions.

- Waiting until tax season to organize financial records — the opposite of proactive tax strategies

If you’re unsure whether your records are in order, E2E Accounting’s Bookkeeping Services can help you stay organized year-round, not just at filing time.

Still have questions about your tax situation?

Every taxpayer’s picture is different. Let our experts review yours.

FAQs: Frequently Ask Question

What are the most common tax deductions that individuals can claim?

The most frequently taken deductions for individuals can include retirement contributions via a plan or IRA, charitable contributions, mortgage interest, or medical costs, education-related expenses, and business expense deductions for those who are self-employed. Each of these deductions will reduce your taxable income and therefore your overall tax liability.

How can retirement contributions help lower taxable income?

Contributions to retirement plans like 401(k)s and standard IRAs are frequently tax-deductible. This means that the amount you contribute is deducted from your taxable income, allowing you to pay less in taxes while also saving for retirement.

What is the difference between a tax deduction and a tax credit?

A tax deduction reduces the amount of income subject to taxation, whereas a tax credit directly reduces the amount of tax owed. Tax credits are often more useful because they reduce your tax liability dollar for dollar.

How does the One Big Beautiful Bill Act affect taxpayers?

The One Big Beautiful Bill Act (OBBBA) modified various tax laws for 2025 and 2026, including increased standard deductions and modified regulations for certain corporate deductions and depreciation. This makes year-end tax planning even more critical.

Conclusion

Effective planning with regard to how you will treat your taxes can significantly affect your overall out-of-pocket amount that you end up paying in taxes. In addition to being able to lower your tax liability which, in turn, improves your financial situation, you can legally reduce the total amount of taxes that you will owe by understanding applicable deductions, utilizing tax-preferred vehicles, and making well-thought-out financial decisions throughout the year.

Tax planning in advance is much more productive than searching for available deductions at the last minute; therefore, as part of your regular financial review, the ability to maintain accurate records and stay current on tax law changes can help you to maximize your tax savings while avoiding unnecessary expenses.

Regardless of your employment status as an employee, investor, self-employed, or owner of a business, implementing the most appropriate tax strategies for your circumstances can enable you to retain more of your income in compliance with the applicable tax laws.